Should you invest or pay off debt first? Learn how to evaluate credit card debt, investing opportunities, and the tradeoffs that affect long-term wealth.

Credit card debt is becoming increasingly common. According to a recent CNBC report citing data from the New York Federal Reserve, Americans now carry a record $1.25 trillion in credit card debt. At the same time, inflation, higher interest rates, and market volatility have made many financial decisions feel less straightforward than they did just a few years ago.

Which raises an important question: Should you prioritize investing or paying off debt first?

The answer, like most financial planning questions, is: it depends.

The good news is this usually isn’t an either-or decision, but the opportunity costs should be considered.

For young professionals and families in the wealth accumulation phase, we want to understand the interplay of investing, debt payoff, cash flow, retirement, and other long-term planning. The objective is not simply to eliminate debt as quickly as possible or invest every extra dollar, but to make financial decisions that strengthen your overall financial position over time.

Understanding the Tradeoff

Investing and paying off debt are both ways of improving your financial future, but they work very differently.

When you invest, you’re putting money toward future growth. You’re giving your money the opportunity to grow and compound over time to build long-term wealth.

Debt works in the opposite direction. Instead of money growing for you, compound interest is working against you.

Credit card debt is particularly challenging because interest rates are so high and can snowball quickly. If you carry a balance month-to-month, interest gets added to the balance, which means you’re paying interest on top of interest. When doing the math, I often see credit card minimum payments are barely higher than the amount of interest accrued that month! No wonder paying off credit card debt can feel like a losing battle.

That’s why the question isn’t simply “Should I invest or pay off debt?” but instead:

Where will your next dollar have the greatest long-term impact?

Opportunity Cost

This is where we revisit the concept of opportunity cost. Opportunity cost is the value of the next-best alternative you give up when making any choice. It is a concept I continuously point to when creating financial plans with clients. There is usually a “best” decision when it comes to the way the numbers will shake out in the end. However, there is usually also a peace-of-mind decision that doesn’t always line up with the numbers decision.

Sometimes the decision that helps you sleep better at night is just as valuable as the one that results in more dollars long-term.

When Investing May Make More Sense

As a general rule, investing may make sense when your expected long-term investment return is meaningfully higher than the interest rate on your debt.

For example:

- A mortgage at 5%

- A diversified long-term investment portfolio expected to return 8% over time

In this situation, continuing to invest while making regular loan payments could potentially create greater long-term wealth.

This is especially true when:

- You have a stable emergency fund

- You are already contributing to retirement accounts

- Your debts have relatively low interest rates

- You have a long investment time horizon

- Your mortgage interest is tax-deductible (meaning you itemize your deductions), reducing your effective interest rate

That said, investing always involves risk. Markets fluctuate. Some years provide high returns, while in other years, portfolio values can decline. Long-term growth is never guaranteed, even when history provides useful context. Debt, on the other hand, is reliably going to cost as much as the stated interest rate indicates (though it should be noted that some debts, particularly credit cards and HELOCs, are typically variable and go up and down as interest rates change).

Your comfort with volatility matters too. Some investors can stay disciplined through market swings, while for others, watching account balances move up and down causes significant worry and anxiety.

A good financial plan should account for both math and peace-of-mind.

Why High-Interest Debt Often Comes First

Credit card debt changes the equation. As of 2026, many credit cards still carry interest rates near or above 20%. Few investments can reliably outperform that level of guaranteed borrowing cost over time.

Paying down high-interest debt can effectively provide a “risk-free-return” equal to the interest rate you eliminate. For example, paying off a credit card charging 22% interest is similar to earning a guaranteed 22% return on your money.

High-interest debt can also impact:

- Cash flow

- Your credit score

- Future borrowing costs

- Mortgage qualification

- Financial flexibility

One major factor in your credit score is your credit utilization ratio, or how much available credit you’re currently using. Maxed-out cards can significantly hurt your score, while lowering balances typically improves it over time.

And beyond the numbers, debt can carry emotional weight. Even if investing may technically offer a higher expected return, many people value the peace-of-mind that comes from reducing financial stress and simplifying cash flow.

The Best Strategy for Many People: Do Both

Paying off debt and investing are not mutually exclusive goals. In fact, many households benefit most from a balanced strategy that allows them to:

- Continue building long-term wealth

- Pay extra toward high-interest debt

- Build an emergency fund

One of the most common examples is maintaining an emergency fund while paying down debt aggressively.

Without emergency savings, even small unexpected expenses can push people deeper into credit card debt. That’s why building liquidity is often a foundational step in a strong financial plan.

A high-yield savings account or money market fund can be a good place to keep emergency reserves while still maintaining accessibility and stability.

Another good place to invest money even while focusing on paying down debt is in an employer-sponsored retirement plan, particularly if the employer provides a match. If you contribute 3% and your employer matches 3%, that is a 100% return. This is the best return you’re likely to find on a consistent basis!

Some clients have said they are more motivated to pay off credit card debt and reduce spending when they continue investing at the same time, because their overall financial situation feels more well-rounded.

That is one reason why financial planning is rarely all-or-nothing.

A Smarter Way to Pay Off Debt

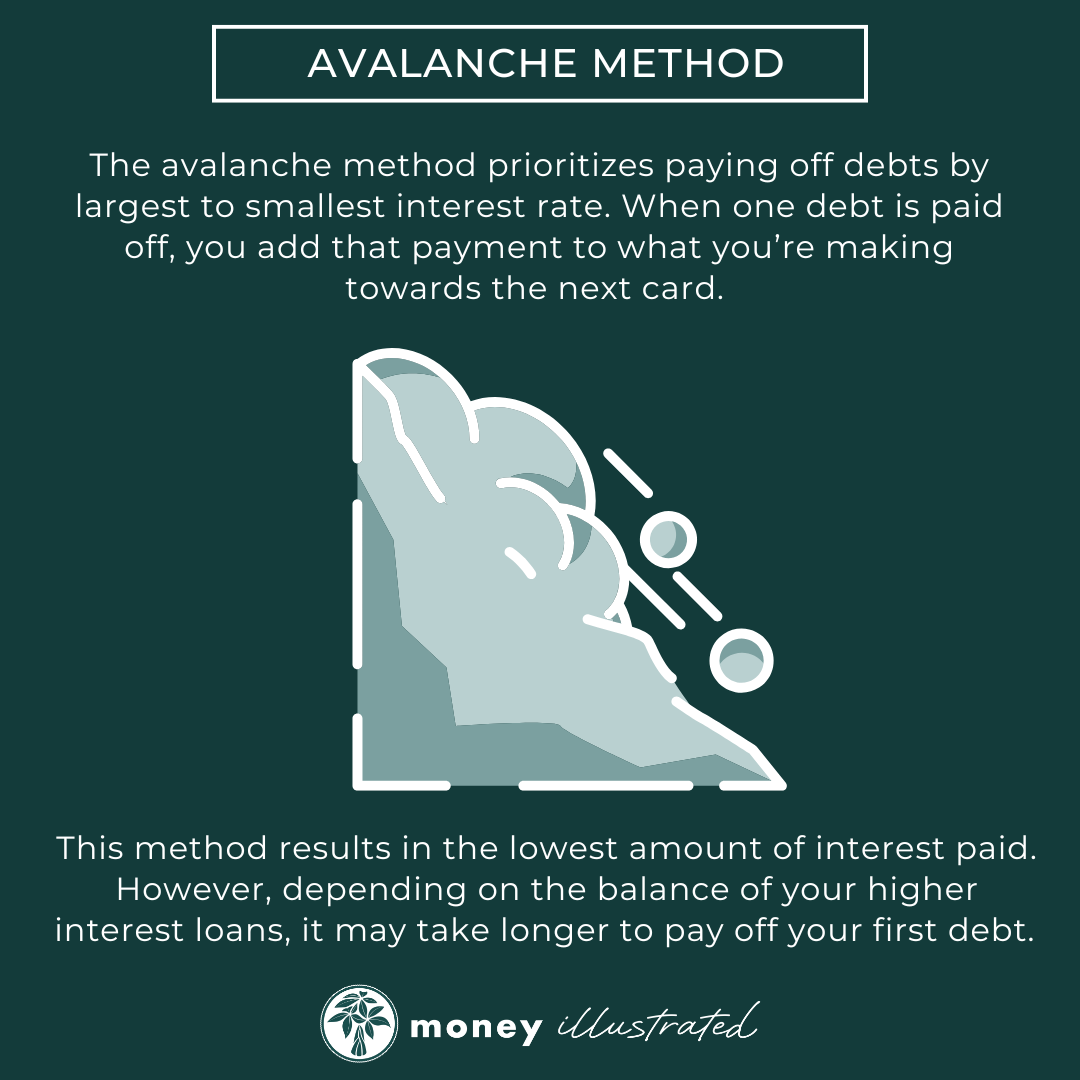

In most cases, the best mathematical strategy is to:

- Make minimum payments on all debts

- Direct any extra cash toward the highest interest rate first

- Continue until that balance is eliminated

- Roll those payments into the next highest-rate debt

This approach is commonly known as the debt avalanche method.

Other Options to Consider

Depending on your situation, there may be additional strategies worth exploring.

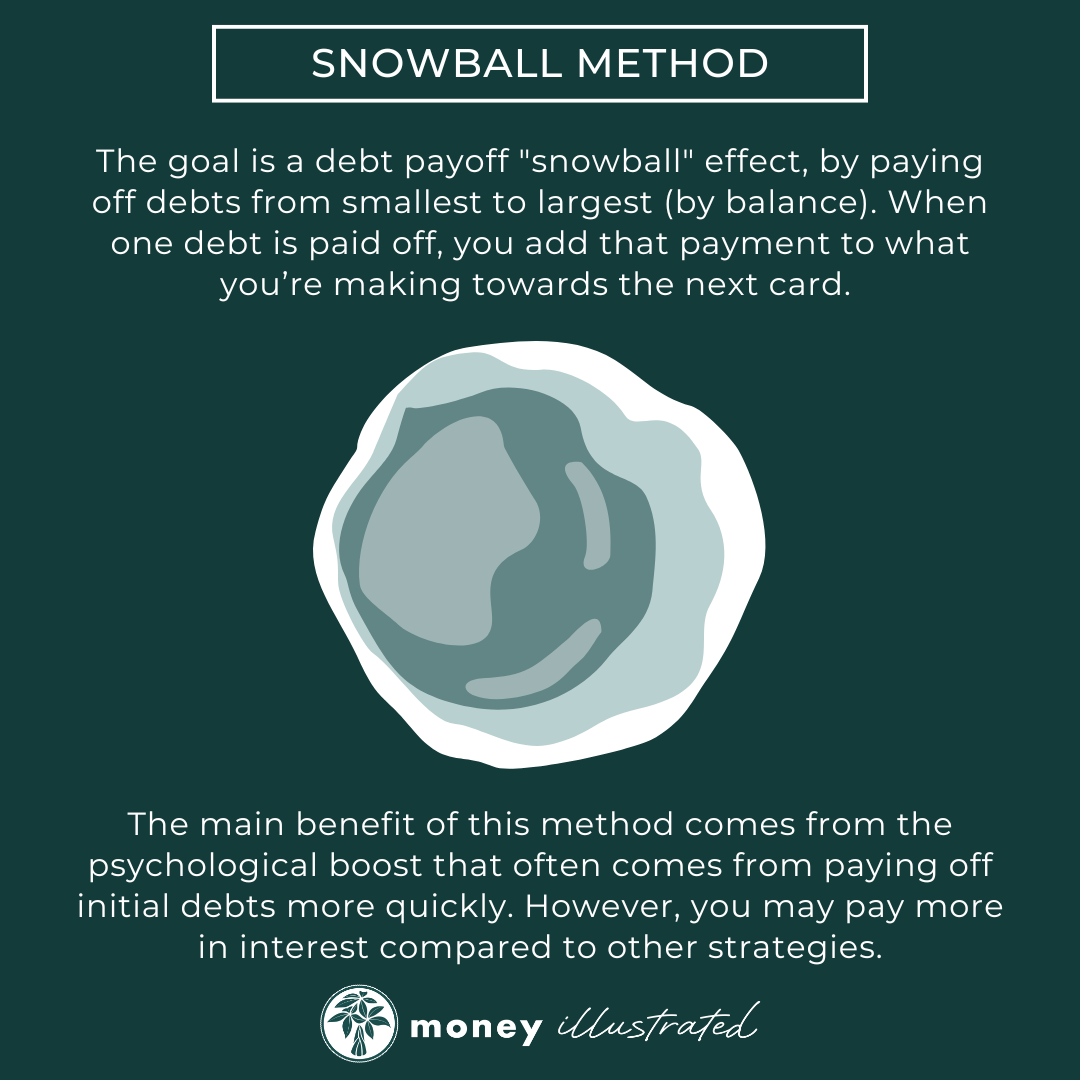

Snowball Method: In this approach, you pay off the smallest balance debt first. Sometimes the psychological win can be more motivating than the avalanche method.

Balance Transfer Cards: Some credit cards offer promotional 0% interest periods for 6-18 months. When used carefully, these can help accelerate debt payoff by temporarily reducing interest costs.

Debt Consolidation Loans: Consolidating multiple debts into one loan may simplify payments and potentially lower your interest rate. Be cautious when using this option, as there are many predatory lenders offering consolidation loans.

Negotiating with Lenders: If minimum payments have become difficult to manage, contacting your lender early on is important. Some providers may offer hardship programs, modified payment plans, or temporary rate reductions.

A Practical Rule of Thumb

While every situation is unique, a reasonable general guideline is:

- If your debt interest is above roughly 5-6%, prioritize paying it down more aggressively, particularly if it is non-mortgage debt.

- If your debt is below that range, continuing with investing while making regular payments may make more sense

Of course, this depends on:

- Emergency savings

- Income stability

- Risk tolerance

- Retirement goals

- Time horizon

- Tax considerations

- Overall cash flow

The right answer is rarely found in a headline or social media post. It comes from viewing your financial life as an integrated system rather than isolated decisions.

Bottom Line

The goal isn’t simply to eliminate debt or maximize investing. The goal is to build long-term financial flexibility and confidence. For many people in the wealth accumulation phase, that means:

- Eliminating high-interest debt strategically

- Continuing to invest consistently

- Maintaining liquidity for unexpected expenses

- Building a plan aligned with long-term goals

When debt payoff and investing work together instead of competing with each other, your financial progress becomes much more sustainable.

If you have questions about prioritizing debt, investing, or creating a strategy tailored to your goals, we’d be happy to help you think through the tradeoffs and build a plan that fits your situation. Schedule a complimentary consultation call here.

Sources

APA: CNBC. (2026, May 12). New York Fed: Credit card debt stands at $1.25 trillion. CNBC. https://www.cnbc.com/2026/05/12/new-york-fed-credit-card-debt-stands-at-1point25-trillion.html